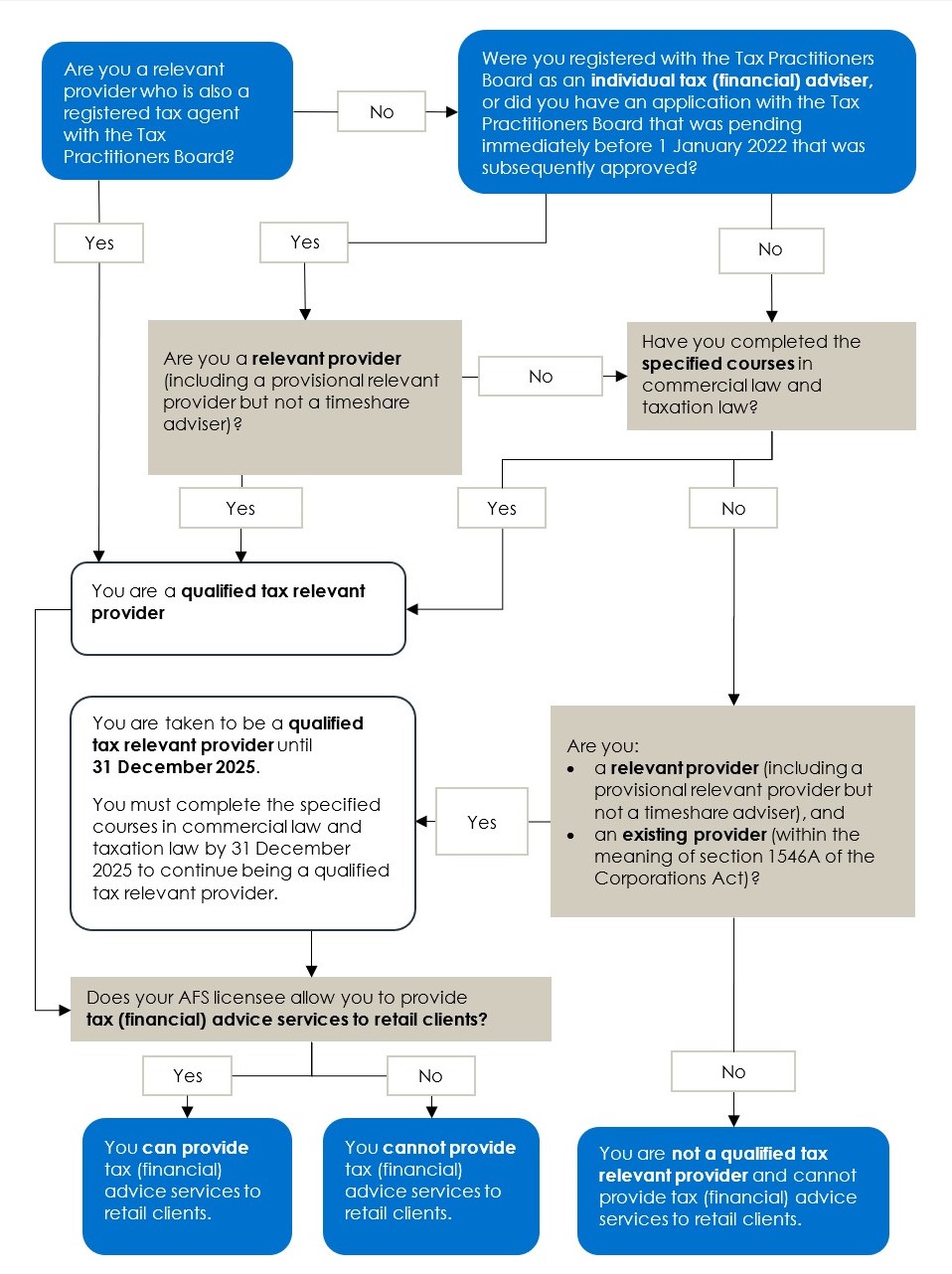

Flowchart: Providing tax (financial) advice services

This flowchart should be read with Information Sheet 268 Relevant providers who provide tax (financial) advice services (INFO 268). It sets out how to determine if you can provide tax (financial) advice services to retail clients as a relevant provider.

Flowchart: Providing tax (financial) advice services

Note: See text version of flowchart process below which includes links to further information.

Text version – Flowchart: Providing tax (financial) advice services

|

Step number |

Step information |

|

Step 1 |

Are you a relevant provider who is also a registered tax agent with the Tax Practitioners Board?

|

|

Step 2 |

Were you registered with the Tax Practitioners Board as an individual tax (financial) adviser, or did you have an application with the Tax Practitioners Board that was pending immediately before 1 January 2022 that was subsequently approved?

|

|

Step 3 |

Are you a relevant provider (including a provisional relevant provider but not a timeshare adviser)?

|

|

Step 4 |

Have you completed the specified courses in commercial law and taxation law? For more information, see INFO 268.

|

|

Step 5 |

You are a qualified tax relevant provider. Go to Step 7. |

|

Step 6 |

You are not a qualified tax relevant provider and cannot provide tax (financial) advice services to retail clients. Flowchart path ends. |

|

Step 7 |

Does your AFS licensee allow you to provide tax (financial) advice services to retail clients?

|

|

Step 8 |

You can provide tax (financial) advice services to retail clients. Flowchart path ends. |

|

Step 9 |

You cannot provide tax (financial) advice services to retail clients. Flowchart path ends. |