This is Information Sheet 209 (INFO 209). It summarises the findings of REP 452 and the implications for investors and listed entities.

On 26 October, we released Report 452 Review of high-frequency trading and dark liquidity (REP 452), examining the effect of high-frequency trading and dark liquidity on Australian equity markets. REP 452 also looks at high-frequency trading on our futures exchange market.

- Background

- What is high-frequency trading and dark liquidity?

- Why is ASIC reviewing high-frequency trading and dark liquidity?

- Findings of the reviews

- What this means for investors and listed entities

Background

The reviews indicate that our markets (in exchange products) are generally of high quality and integrity. The current levels of high-frequency trading and dark liquidity do not appear to be adversely affecting the function of these markets or their ability to fulfil their role for the real economy – for businesses and investors. The current regulatory settings are adequate and effective. We will continue to monitor developments to ensure this remains the case.

REP 452 is intended to give investors and listed entities access to greater and more objective information about the effect of high-frequency trading and dark liquidity on Australian markets. Our findings should give them more comfort about the quality and integrity of our markets and enhance their confidence and trust in these markets.

We think that our report will also assist investors to equip themselves to operate in a continually evolving electronic and high-speed environment, and help to inform their choices about where and how their orders are executed.

What is high-frequency trading and dark liquidity?

High-frequency trading

High-frequency trading is not a technical term. High-frequency traders, like many other market users, use computer algorithms to generate buy and sell orders on markets such as ASX and Chi-X. In fact, markets are now highly automated – with the vast majority of orders generated and executed by computer algorithms.

These algorithmic orders can be entered and amended a lot faster than orders generated by people. While it is often equated with algorithmic trading – and high-frequency trading is indeed a type of algorithmic trading – not all forms of algorithmic trading can necessarily be described as high frequency.

One way in which high-frequency trading does differ from other trading is that it tends to seek to profit from incremental price differences between markets and products, rather than to look for underlying value.

Algorithms used by high-frequency traders are generally more sophisticated and able to quickly process information from a variety of sources in order to make trading decisions for that particular strategy (e.g. the price and volume for an order that should be entered, amended or cancelled). In the analysis we have used to support our findings in REP 452, we identified various metrics that distinguished high-frequency trading from other trading methods.

Dark liquidity

Exchange markets, such as ASX and Chi-X, offer 'lit' order books, where buy and sell orders are visible and accessible to the rest of the market before they are executed.

Dark liquidity refers to buy and sell orders that are not visible to the rest of the market, although the trades that result from those orders are typically published immediately after they take place. Dark trades can occur on dark venues operated by exchanges (e.g. ASX's Centre Point and Chi-X's hidden orders, which are offered by these operators in addition to their 'lit' order books). They can also occur away from exchange markets where they are accessible only to a subset of the market (e.g. often limited to a market participant and its clients). A crossing system is a dark venue which is operated away from an exchange, typically by a market participant.

Why is ASIC reviewing high-frequency trading and dark liquidity?

High-frequency trading and dark liquidity have been two of the most topical market structure issues globally in recent years.

During this time, there have been enormous advances in technology within our markets. At the same time, the venues on which trading occurs have also experienced significant developments. Exchange markets have expanded their dark trading facilities while market participant-operated crossing systems have continued to evolve.

In 2012, ASIC analysed the effect of high-frequency trading and dark liquidity on the quality and integrity of our equity markets. Those reviews culminated in Report 331 Dark liquidity and high-frequency trading (REP 331). We also introduced a number of ASIC market integrity rules to address the concerning behaviour we had observed, particularly with crossing systems.

During 2015, we undertook new reviews on high-frequency trading and dark liquidity to build on our earlier analysis. We engaged with industry and regulators here and overseas, analysed market data and reviewed relevant academic research.

Findings of the reviews

High-frequency trading

Negative sentiment about high-frequency trading appears to have tapered off since 2012. Market users have become better informed and equipped to operate in an electronic and high-speed environment. However, some concerns remain and are discussed in this section.

Findings

We analysed order and trade data from the ASX, Chi-X and ASX 24 markets to identify the nature, extent and effect of high-frequency trading in the Australian equity market and in the most traded futures contracts on ASX 24 – the S&P/ASX 200 Index Futures Contract (SPI) and Three Year and Ten Year Commonwealth Treasury Bond Futures Contracts (bond futures).

Presence of high-frequency trading

Our analysis shows that high-frequency trading in equity markets has remained reasonably steady at around 27% of total equity market turnover. This is comparable to levels in Canada, the European Union and Japan. However, it is more concentrated (with 30% fewer high-frequency traders) and high-frequency traders are more active in mid-tier securities than they were in 2012.

For futures, there has been rapid growth in high-frequency trading (from a low base). It has more than doubled over the past year to 21% of turnover in the SPI and 14% of bond futures: see Table 1. While these levels are not currently concerning, we are closely monitoring the growth of high-frequency trading.

Table 1: High-frequency trading in our markets - March quarter 2015

| Measure | Equities | SPI | Bond futures |

| Trading accouts | <0.5% | 2% | 4% |

| Turnover | 27% | 21% | 14% |

| No. of trades | 31% | 25% | 24% |

| No. of orders | 47% | 30% | 40% |

Perceptions of high-frequency trading

As with our 2012 review, we found that some of the commonly held negative perceptions about high-frequency trading were not supported by our analysis. For example, the perception that these traders only hold their positions for a matter of seconds and that they place and cancel orders excessively remains unsupported. We found that, in the March quarter 2015:

- on average, they held their positions for 52 minutes (equities), 31 minutes (SPI) and 39 minutes (bond futures), and

- there are relatively few small and fleeting orders (i.e. that do not rest in the market for any meaningful period of time).[1] Less than 1% of all equity and bond futures orders were small and fleeting. This was more prevalent in the SPI, with 5% of all orders (high-frequency traders accounted for 48%). We are working with market participants to reduce small and fleeting orders in the SPI.

Predatory trading

Where trading is undertaken to exploit others or unfairly induce others to trade, it is often referred to as 'predatory trading'. Predatory trading does not appear to be excessive in our market, but we do investigate instances where there may be a breach of the law. Examples of predatory trading we identified in our markets include:

- a persistent 'pinging' strategy[2] in a highly-traded security on the ASX market. Subsequent inquiries by ASIC led to this behaviour ceasing. We engaged with investors and the underlying listed entity during these inquiries, and

- 'latency arbitrage', which relies on a speed advantage to detect differences between lit exchange markets and dark venues. It can result in investors' dark orders executing at worse prices than on lit markets. We estimated the daily revenue generated by traders on this basis was around $1,100 per day ($285,000 per year), which is not large by other market standards.

Some institutional investors have become more sophisticated, increasingly managing their own order flow and execution decisions so they can limit interaction with predatory traders and improve their trading outcomes.

Revenue earned

There has been commentary here and abroad about excessive revenue earned by high-frequency traders. To help inform this debate, we estimated the gross trading revenue of high-frequency traders in equity markets. Over the 12 months to 31 March 2015, our analysis indicated that this figure was approximately $110–180 million in aggregate.

This translates to a cost of 0.7 to 1.1 basis points (0.007-0.011%) to other users of the market. This is material but substantially less than other figures suggested by some, and less than some other costs in the market (e.g. average bid–offer spreads are 13 basis points). We also noted that high-frequency trading represents approximately 50% of the resting orders around the best price, which suggests that high-frequency traders may be contributing to filling gaps in short-term supply and demand. Where this occurs, high-frequency traders can provide a benefit to wider market users.

Crowding out of quarterly futures expiries

We are conducting inquiries into a small number of traders that were 'crowding out' other users in the 'roll market' on quarterly expiries. This strategy involved excessive order entry and cancellation, resulting in higher costs for other market users. We have asked ASX to consider additional steps to discourage this practice.

Volatility

While high-frequency traders' share of turnover was largest in securities with the most short-term price volatility, they did not appear to exacerbate this volatility.

Dark liquidity

Stakeholder feedback indicates that industry is generally less concerned about dark liquidity in our markets compared to the time of our 2012 review. There are, however, some concerns about existing practices overseas being imported into Australian markets, particularly around the profiling and segmentation of liquidity.

Findings

Share of dark liquidity

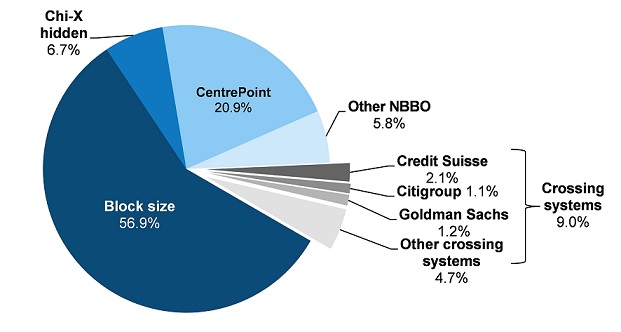

Dark liquidity has remained reasonably constant in recent years at around 25–30% of total equity market turnover. However, its composition continues to change.

In part as a result of rule changes made by ASIC, there has been a partial shift back to using dark liquidity for large block trades (i.e. the original purpose of dark liquidity), which accounted for 56.9% of total dark turnover in the March quarter 2015: see Figure 1. At the same time, there are fewer small dark trades and they are now fairer, with any improvement to prices (compared to lit exchange markets) needing to be more equitably shared between counterparties (which was also required by the trade with price improvement ASIC market integrity rule).

Figure 1: Share of dark liquidity – March quarter 2015[3]

Dark exchange markets

Trading on exchange dark venues (i.e. ASX Centre Point and Chi-X hidden orders) accounted for around twice the total dark trading in 2015 compared to 2012, at 27.6%. Consistent with ASIC's expectations, the growth in trading on exchange dark venues followed the introduction of ASIC's trade with price improvement rule in 2013. This rule requires small dark trades to be done at better prices than available on lit markets. Trading migrated across from crossing systems that were unable to provide this price improvement. Stakeholder feedback also indicated that some institutional investors (e.g. fund managers) have opted out of using crossing systems after experiencing poor price outcomes and information leakage. Others have taken control of their own order routing and execution.

High-frequency traders are active on exchange dark venues, at 14% and 28% of turnover on ASX Centre Point and Chi-X hidden orders respectively. High-frequency traders appear to be achieving a better price than other users of these venues around 85% of the time (on trades where one party achieves a better price outcome).

Crossing systems

In Australia, there are currently 17 crossing systems operated by 15 market participants. They accounted for 9% of total dark turnover in the March quarter 2015 (see Figure 1), almost half of the level in 2012.

Many of the concerning trends with crossings systems that we identified in 2012 have abated. Investor perceptions about the integrity and transparency of crossing systems in our market are more positive. This is largely a result of:

- buy-side clients demanding improved standards from their broker or service provider

- the introduction of ASIC market integrity rules to improve transparency around the operation (and enhance the fairness) of crossing systems, and

- possible improvements made by crossing system operators in response to regulators probing dark pool operators in the United States.

High-frequency traders (according to our measure) are active in 11 crossing systems and account for around 2% of total crossing system turnover. For a small number of these, the crossing system operator indicated to clients and to ASIC that there was no high-frequency trading (it is possible that they have a different definition of high-frequency trading to ours). This is lower than in 2012.

We found that on average across all crossing systems, all users were achieving comparable price outcomes (i.e. high-frequency traders and the crossing system operator were not achieving better outcomes).

Preferencing in equity markets

We have seen a trend here and overseas of exchange and crossing system operators seeking to preference some market users over others (e.g. by providing better or worse order execution priority) for dark trading. These developments could undermine fair and non-discriminatory secondary trading and it may also be inconsistent with operators’ obligations under the Corporations Act 2001 and ASIC market integrity rules. We are unlikely to support further forms of preferencing for this reason.

Principal trading and facilitation

We are concerned about how some market participants are managing conflicts of interest when trading on their own behalf against their clients (either principal trading desks or to facilitate client orders). We have clarified our expectations that:

- participants should avoid situations where staff are responsible for the participant's own trading while having access to unexecuted client order information, and

- additional controls should be put in place (e.g. physical separation of some functions) to manage the conflicts and conduct risk arising.

What this means for investors and listed entities

High-frequency trading

Our analysis shows that, in general, high-frequency trading is not affecting prices or volatility in a material way.

We acknowledge that some people have concerns about predatory trading. While predatory trading does not appear to be excessive in our markets, it can adversely affect trading outcomes for investors. Our priority is ensuring all investors have trust and confidence in our markets, and we will examine instances of predatory trading that may breach the law.

Investors should engage with their brokers to understand how their orders and confidential information are being handled to ensure their interests, and those of any beneficiaries to whom fiduciary obligations are owed, are not compromised.

Dark liquidity

We encourage investors to take advantage of the ASIC market integrity rules introduced in response to our 2012 dark liquidity review, which:

- enable wholesale clients to request that participants disclose when they have traded with their clients as principal (there was already a requirement to disclose this information to retail clients). This helps to manage participants' conflicts of interest and has been widely used by institutional clients, and

- improve transparency around crossing systems (transaction data and disclosure about crossing system operations). Find out more about crossing systems.

As a result of these rules, there has been considerable improvement in disclosure and transparency since our last review. This has contributed to investors regaining confidence and trust in crossing system operators. Investors are now able to make more informed choices about where and how their orders are managed, and listed entities are more informed about where their securities are being traded.

Next steps

We will continue to monitor developments in high-frequency trading and dark liquidity, including the recent exponential growth of high-frequency trading in the futures market and the costs imposed on the market by high-frequency trading compared to the benefits. Our surveillance focus on predatory trading that manipulates the market will continue and we will actively enforce market misconduct laws. We will inform the market of our progress on the quarterly futures expiry issue. We will also continue our forward-looking review of the purpose of markets and their fundamental role in an environment of rapid change.

We encourage investors and listed entities to raise with ASIC any further issues or concerning instances or practices they are observing in the market.

Information sheets provide concise guidance on a specific process or compliance issue or an overview of detailed guidance.

This information sheet was issued in October 2015.

Important notice

Please note that this information sheet is a summary giving you basic information about a particular topic. It does not cover the whole of the relevant law regarding that topic, and it is not a substitute for professional advice. We encourage you to seek your own professional advice to find out how the applicable laws apply to you, as it is your responsibility to determine your obligations.

You should also note that because this information sheet avoids legal language wherever possible, it might include some generalisations about the application of the law. Some provisions of the law referred to have exceptions or important qualifications. In most cases, your particular circumstances must be taken into account when determining how the law applies to you.

[1] Fleeting orders are orders of less than $500 (equities) and one contract (futures) in value and removed from the market in less than half a second.

[2] Pinging is the practice of using the placement of very small orders in dark venues to test if there are other orders.

[3] ‘Block size’ refers to trades executed under the pre-trade transparency exceptions in Rules 4.2.1 and 4.2.2 of the ASIC Market Integrity Rules (Competition in Exchange Markets) 2011 – typically of $1 million ($200,000 for some issuers' shares since May 2013) or more.