Australian financial services (AFS) licensees are required to ensure the information recorded on the Financial Advisers Register about their relevant providers, is accurate and complete. This includes accurately recording how a relevant provider has met the qualifications standard.

To assist AFS licensees and their relevant providers to identify incorrect or outdated information on the Financial Advisers Register, ASIC has made a temporary dataset available.

The dataset includes information on a relevant provider’s capacity to provide tax (financial) advice services, the relevant provider’s qualification and training courses (including whether a particular course or qualification has been marked as going towards the relevant provider meeting the qualifications standard), the date the relevant provider passed the exam and whether their AFS licensee has notified ASIC that the relevant provider is relying on the experienced provider pathway.

This is a point in time dataset, current as at 25 June 2026.

If a relevant provider has been appointed and/or had their details updated on the Financial Advisers Register after ASIC prepared the dataset, the relevant provider’s details may not appear in the spreadsheet.

Important information about this dataset

The information in this dataset is provided by Australian Financial Services (AFS) licensees and/or authorised representatives as required under the Corporations Act 2001 (Cth) and associated regulations.

ASIC does not check or review the information provided before it is published.

If you have any questions about a relevant provider (commonly known as a financial adviser) that are not addressed by this dataset, please contact the relevant business or individual directly.

For further information, including the ability to search for individual relevant provider details, please visit the Moneysmart Financial Advisers Register. The Moneysmart website allows you to look up the details of current and ceased relevant providers, while this dataset provides a summary of information relevant to the qualifications standard and a relevant provider’s ability to provide tax (financial) advice services. The dataset provides information for current relevant providers only.

Industry sometimes uses the terms ‘relevant provider’ and ‘financial adviser’ interchangeably.

Qualification and training information to be recorded on the Financial Advisers Register

Qualifications and training courses completed by a relevant provider that are relevant to the provision of financial services must be recorded on the Financial Advisers Register.

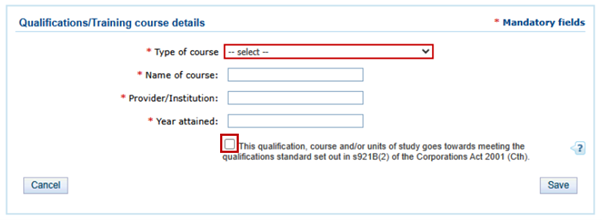

If the relevant provider has met the qualifications standard, all of the qualifications or training courses that go toward the relevant provider meeting the qualifications standard, should be recorded on the Financial Advisers Register. Importantly, these qualifications and courses need to be marked as a ‘qualification, course and/or unit of study that goes towards the relevant provider meeting the qualifications standard as set out in s921B(2) of the Corporations Act 2001 (Cth)’ by selecting the check box, see the example below.

Example

If a relevant provider is an existing provider and has a relevant degree and an advanced diploma of financial planning (ADFP), they are required to complete an Ethics for Professional Advises bridging unit to meet the qualifications standard.

Once the relevant provider has completed the bridging unit, the AFS licensee should mark each of the relevant degree, ADFP and the bridging unit as a ‘qualification, course and/or unit of study that goes towards the relevant provider meeting the qualifications standard set out in s921B(2) of the Corporations Act 2001 (Cth) by selecting the check box.

Figure 1: Screenshot of ASIC Connect: Qualifications/Training course details form

If the AFS licensee is having trouble updating the relevant provider’s qualification and training courses, see the ‘Trouble shooting’ section below.

Any other qualifications or training courses that are relevant to the provision of financial services should also be listed. But if they do not go towards the relevant provider meeting the qualifications standard, they should not be marked as such. Examples of these types of qualifications or training may include the specified courses in commercial law and taxation law or a professional designation (e.g. ‘Certified Financial Planner’).

Checking the information recorded on the Financial Advisers Register

To help AFS licensees and relevant providers determine whether incorrect and/or out of date information is recorded on the Financial Advisers Register, ASIC has provided a one-off, point-in-time dataset.

Relevant providers and AFS licensees are encouraged to check the following information on the dataset.

Qualifications

Confirm whether the relevant provider’s qualifications have been accurately recorded on the Financial Advisers Register. In particular, confirm that:

- If the relevant provider has met the qualification standard via formal qualifications, all of the qualifications or training courses that go toward the relevant provider meeting the qualifications standard, should be recorded on the Financial Advisers Register and be marked as such, (using the check box as in the example above). These courses will be listed in column K of the dataset. See the section on ‘Qualification and training information to be recorded on the Financial Advisers Register’ above for more information,

- If the relevant provider has not met the qualification standard via formal qualifications, and is relying on the experienced provider pathway instead, none of the qualifications or training courses need to be marked as a ‘qualification, course and/or unit of study that goes towards the relevant provider meeting the qualifications standard set out in s921B(2) of the Corporations Act 2001 (Cth).’ These courses will be listed in column L of the dataset.

If the AFS licensee is having trouble updating the relevant provider’s qualification and training courses, see the ‘Trouble shooting’ section below.

Common errors include, AFS licensees:

- marking the exam as a ‘qualification, course and/or unit of study that goes towards the relevant provider meeting the qualifications standard set out in s921B(2) of the Corporations Act 2001 (Cth).’ This is incorrect as the exam goes towards the relevant provider meeting the exam standard set out in s921B(3) of the Corporations Act 2001 (Cth).

- only marking a bridging unit (or some other qualification) as a ‘qualification, course and/or unit of study that goes towards the relevant provider meeting the qualifications standard set out in s921B(2) of the Corporations Act 2001 (Cth).’ These may be listed in the Determination but are required to be coupled with other qualification(s) to meet the requirements of the professional standard.

- only marking a professional designation (e.g. ‘Certified Financial Planner’) as a ‘qualification, course and/or unit of study that goes towards the relevant provider meeting the qualifications standard set out in s921B(2) of the Corporations Act 2001 (Cth).’

The AFS licensee should also pay close attention to how the particulars of the qualification, course or unit of study was entered onto the Financial Advisers Register. ASIC has previously provided guidance on how to assess a relevant provider’s qualifications and enter these particulars onto the Financial Advisers Register, including:

Experienced provider pathway (EPP) declarations

Before the AFS licensee notifies ASIC of a relevant provider’s EPP declaration they should confirm that the relevant provider is eligible to rely on the EPP.

If the relevant provider is relying on the EPP, confirm whether this information is accurately recorded in column M of the dataset. If the information recorded in column I of the dataset is:

- “N” or “blank” the AFS licensee has not notified ASIC that the relevant provider is relying on the EPP. The AFS licensee is required to confirm that the relevant provider has met the qualifications standard through formal education and ensure that this information is accurately recorded on the Financial Advisers Register (see Qualifications above).

- “Y” the AFS licensee has notified ASIC that the relevant provider is relying on the EPP. The AFS licensee should confirm that the relevant provider has met the eligibility criteria as outlined in Information Sheet 281 Accessing the experienced provider pathway (INFO 281). If the relevant provider does not meet the eligibility criteria as outlined in INFO 281, the AFS licensee should:

- submit a maintain (update) transaction to notify ASIC that the relevant provider is not relying on the EPP, and

- confirm whether the relevant provider has met the qualifications standard through formal education and ensure this information is accurately recorded on the Financial Advisers Register (see Qualifications above).

QTRP Capacity

Confirm whether the relevant provider has met the definition of ‘qualified tax relevant provider’ and is able to provide tax (financial) advice services. Check this information in the dataset:

- whether the relevant provider is able to provide tax (financial) advice services as recorded in column H of the dataset; and

- the capacity in which the relevant provider can provide tax (financial) advice services as recorded in column I of the dataset.

Blank in Column H

If column H is blank, the AFS licensee has not notified ASIC as to whether the relevant provider can provide tax (financial) advice services. The AFS license is required to submit a maintain (update) transaction and notify ASIC of whether or not the relevant provider can provide tax (financial) advice services.

“N” in Column H

If column H contains a “N”, the AFS licensee notified ASIC that the relevant provider cannot provide tax (financial) advice services. If this information is correct, no further action is required. If this information is incorrect, the AFS licensee is required to:

- confirm whether the relevant provider is a registered tax agent or has completed the specified commercial law and taxation law courses, and

- submit a maintain (update) transaction to notify ASIC that the relevant provider can provide tax (financial) advice services and the capacity in which they can do so.

“Y” in Column H

If column H contains a “Y”, the AFS licensee notified ASIC that the relevant provider can provide tax (financial) advice services. The AFS licensee is required to confirm that the information in column I (which is the capacity in which the relevant provider can provide tax (financial) advice services) is accurate. The only valid responses for column I, as at 1 January 2026, are:

- “The financial adviser is a relevant provider who was registered as an individual tax (financial) adviser with the Tax Practitioners Board immediately before 1 January 2022”;

- “The financial adviser's application for registration as an individual tax (financial) adviser with the Tax Practitioners Board was approved post 1 January 2022”;

- “The financial adviser has completed the specified commercial law and taxation law courses”; and

- “The financial adviser is a registered tax agent with the Tax Practitioners Board”.

If this information is correct, no further action is required.

If column I contains any of the following responses, the AFS licensee is required to take submit a maintain (update) transaction:

- “The financial adviser is also an existing provider; from 1 Jan 2026 they must have completed the specified commercial law and taxation law courses” or

- “The financial adviser is an existing provider who was a relevant provider immediately before 1 Jan 2022 and has not passed the FA exam; from 1 Oct 2022 they must have passed the FA exam, completed the prescribed commercial law and taxation law courses” or

- Blank

The update required by the AFS licensee depends on whether the relevant provider is able to provide tax (financial) advice services and the capacity in which they can do so.

- If the relevant provider is able to provide tax (financial) advice services:

- confirm whether the relevant provider is a registered tax agent or has completed the specified commercial law and taxation law courses; and

- submit a maintain (update) transaction to notify ASIC that the relevant provider can provide tax (financial) advice services and the capacity in which they can do so.

If the relevant provider is not able to provide tax (financial) advice services, submit a maintain (update) transaction to notify ASIC that the relevant provider cannot provide tax (financial) advice services

Updating information recorded on the Financial Advisers Register

Relevant providers cannot update the Financial Advisers Register themselves. A relevant provider’s authorising AFS licensee is required to update the information recorded on the Financial Advisers Register by submitting a maintain (update) transaction via ASIC Connect.

AFS licensees have 30 business days to notify ASIC of a change to a relevant provider’s details and can do this by lodging a Maintain transaction via ASIC Connect.

Trouble shooting

ASIC is aware that some AFS licensees have had issues with updating the relevant provider’s details in ASIC Connect.

If a qualification or training course was previously entered, and now needs to be amended, the system requires AFS licensees to remove the qualifications and training course from the form, and then add the course again with the correct details. Importantly, this includes where the course needs to be updated to change whether it’s marked as a ‘qualification, course and/or unit of study that goes towards the relevant provider meeting the qualifications standard as set out in s921B(2) of the Corporations Act 2001 (Cth)’, using the check box, as in the example above.

If the AFS licensee is having trouble loading the ASIC Connect webpage, they should also consider clearing their cache and cookie data, as this may help with the loading time of the web page. If the issue persists, please notify ASIC by reporting a technical issue.

Additional resources

ASIC has published various resources to assist AFS licensees and their relevant providers by providing information on how to assess a relevant provider’s transcripts against the Determination and how to enter this information onto the Financial Advisers Register.