Equity market data for quarter ending June 2023

For an explanation of the measures used in this release, see Information Sheet 177 Quarterly cash equity market data: Methodology and definitions (INFO 177).

Summary

Tables

Table 1: Market characteristics – average for June quarter 2023

Table 2: Measures of market concentration

Table 3: Measures of market efficiency

Graphs

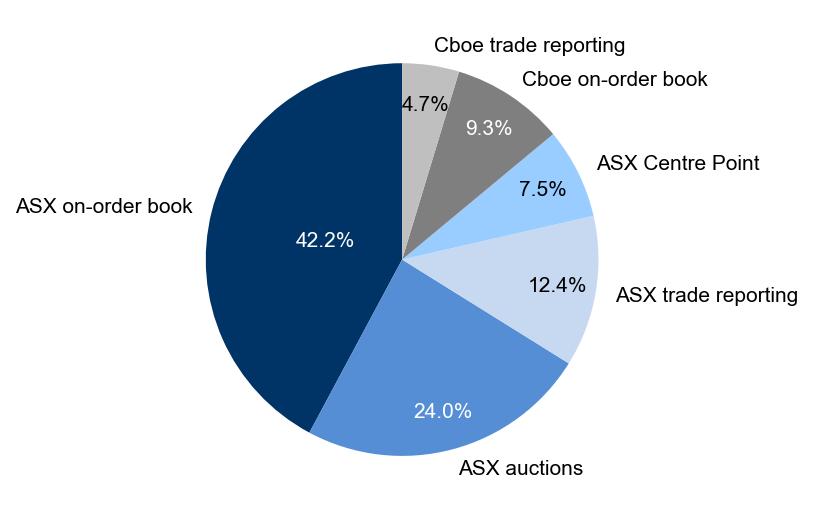

Figure 1: Market share – June quarter 2023

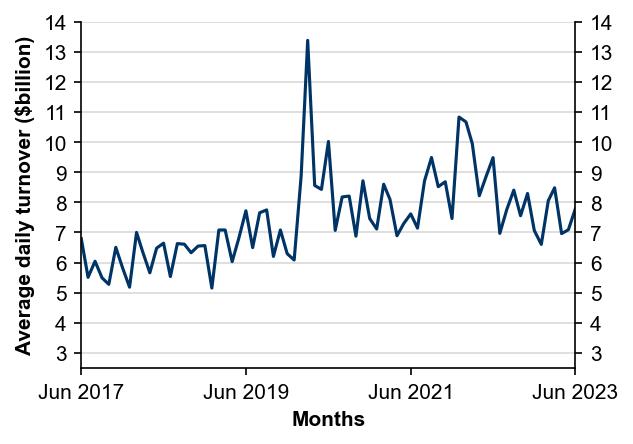

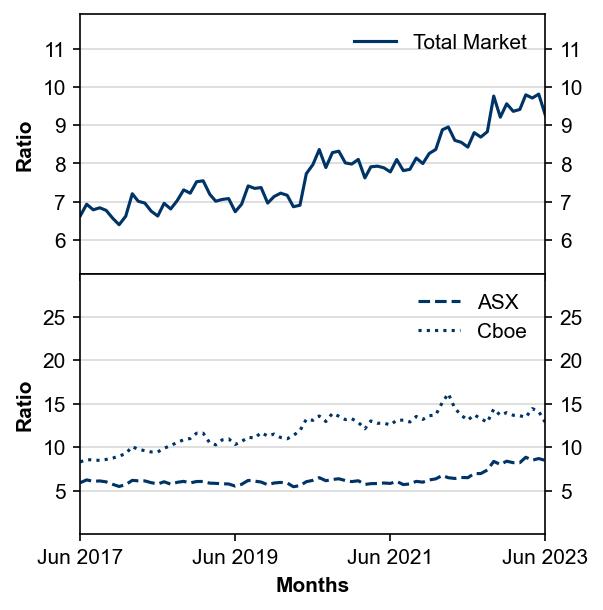

Figure 2: Average daily turnover

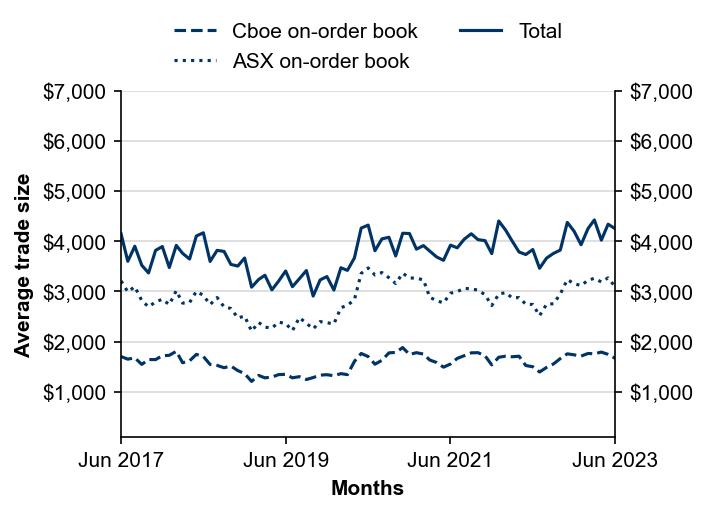

Figure 3: Average trade size by execution venue

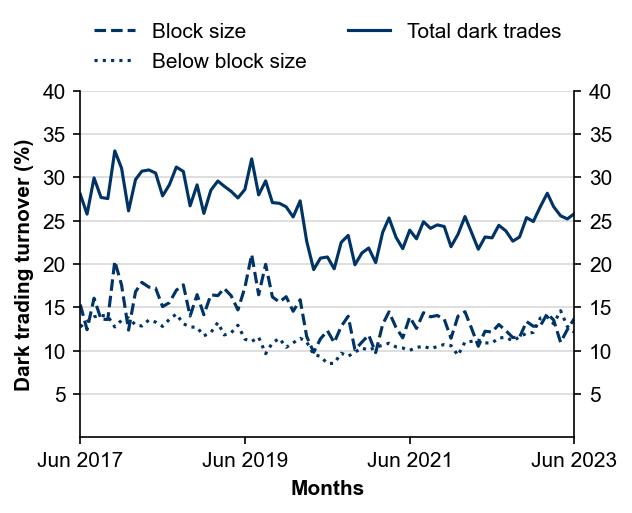

Figure 4: Dark liquidity proportion of total value traded

Figure 5: Order-to-trade ratio

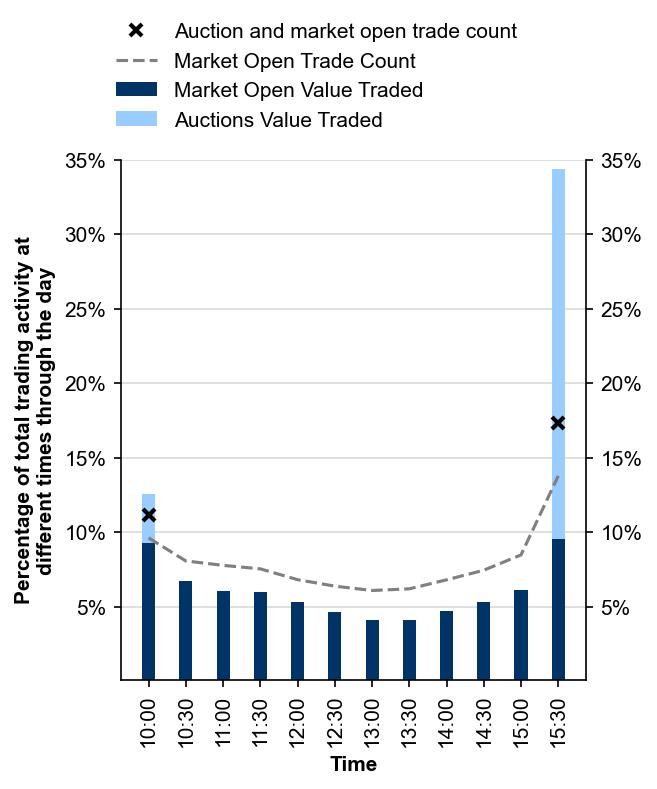

Figure 6: Intraday trading profile – June quarter 2023

Figure 10: Effective bid–ask spreads

Equity market data from other quarters

Summary for quarter ending June 2023

In the June 2023 quarter, ASX accounted for 86.0% of the total dollar turnover in equity market products. Cboe accounted for the remaining 14.0% of total dollar turnover. This is an increase in ASX’s market share from last quarter where it was 81.6%. These figures include all trades executed on order book, as well as trades matched off order book and reported to either market operator. On order book turnover (excluding ASX auctions) as a proportion of total dollar turnover decreased to 58.9% in the June quarter from 60.8% in the March quarter. Trade reporting turnover as a proportion of total dollar turnover decreased to 17.1%, compared to 18.0% in the March quarter.

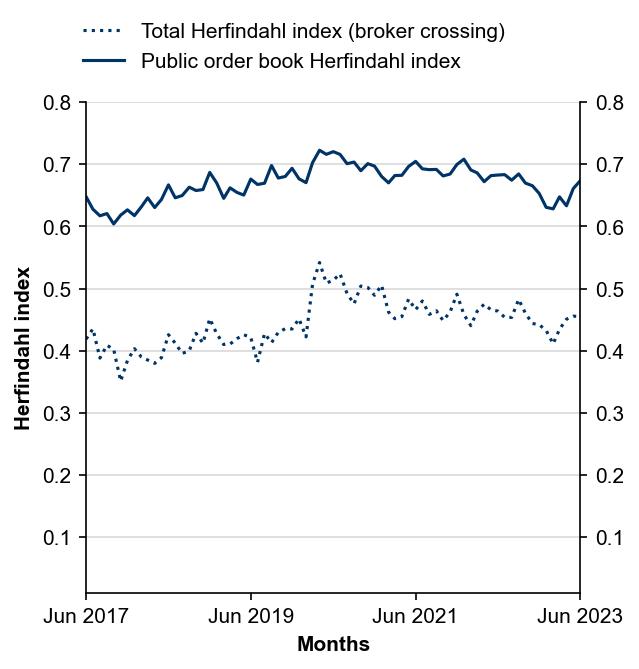

ASX’s market share, measured by the Herfindahl-Hirschman Index (HHI) measure of market concentration of public order book volumes, increased to 0.66 in the June quarter from 0.64 in the March quarter (maximum 1.00).

Daily Turnover in the Australian equity market decreased by $0.4 billion from the March quarter to an average of $7.3 billion for the June quarter.

The overall order-to-trade ratio increased from 9.5:1 in the March quarter to 9.6:1 in the June quarter.

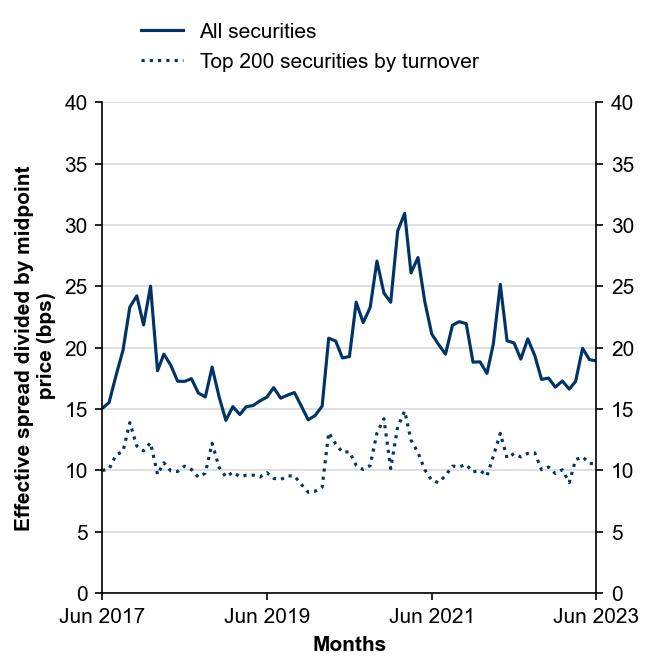

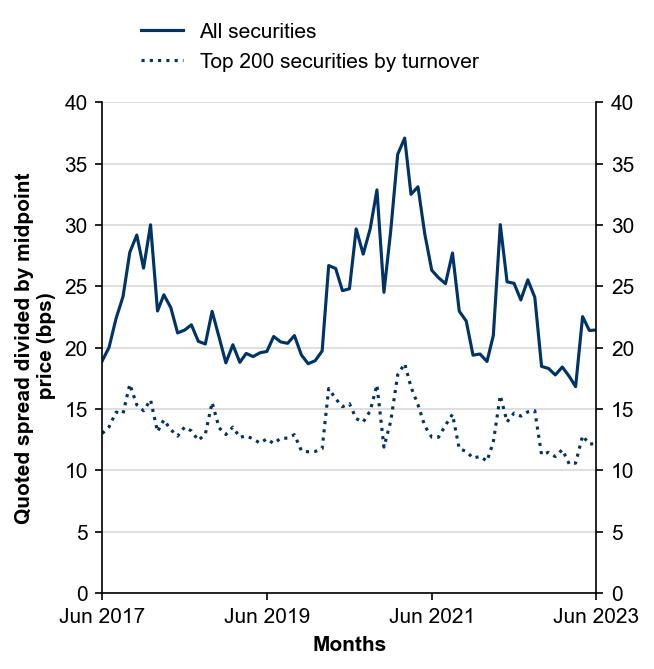

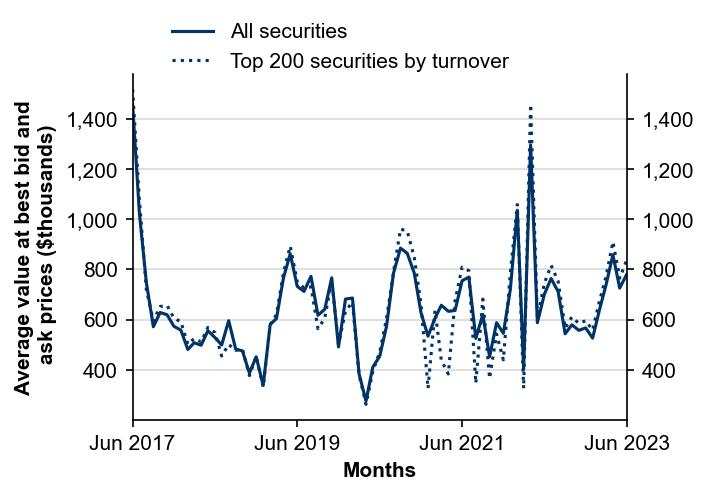

Depth of the orderbook across the best bid and ask in the June 2023 quarter reached an average of $837,000 across the largest 200 securities and $788,000 across all securities, compared to $668,000 and $635,000 last quarter, respectively. Quoted spreads in the June quarter have increased for the largest 200 securities, currently at an average of 12.39 bps from 10.93 bps last quarter. Across all securities, quoted spreads have increased, at 21.79 bps from 17.63 bps last quarter. Effective spreads have increased across the largest 200 securities, at 10.73 bps from 9.97 bps last quarter, and increased across all equity products, at 19.30 bps in the June quarter from 17.05 bps previously.

Table 1: Market characteristics – average for June quarter 2023

| Statistics | ASX on book | ASX Auctions | ASX Centre Point | ASX trade reporting | Cboe on book | Cboe trade reporting | Total |

|---|---|---|---|---|---|---|---|

| Number of trades per day | 965,281 | 61,568 | 205,446 | 48,534 | 389,651 | 62,125 | 1,732,607 |

| (market share) | 55.7% | 3.6% | 11.9% | 2.8% | 22.5% | 3.6% | 100.0% |

| Value traded ($ million/day) | 3,070.3 | 1,744.3 | 542.5 | 906.0 | 675.9 | 341.2 | 7,280.4 |

| (market share) | 42.2% | 24.0% | 7.5% | 12.4% | 9.3% | 4.7% | 100.0% |

| Order-to-trade ratio | 8.6 | na | 6.7 | na | 13.8 | na | 9.6 |

| Average trade size ($/trade) | 3,184.5 | 28,305.5 | 2,647.1 | 19,596.3 | 1,735.9 | 5,487.6 | 4,203.6 |

Table 2: Measures of market concentration

| Statistics | Jun 2022 | Apr 2023 | May 2023 | Jun 2023 |

|---|---|---|---|---|

| Total market | 0.46 | 0.45 | 0.46 | 0.46 |

| Public venues | 0.68 | 0.63 | 0.66 | 0.67 |

Table 3: Measures of market efficiency

| Market Efficiency Statistics | Jun 2022 | Apr 2023 | May 2023 | Jun 2023 |

|---|---|---|---|---|

| Quoted bid-ask spread (bps) | ||||

| Top 200 securities by turnover | 14.67 | 12.82 | 12.14 | 12.19 |

| All Securities | 25.24 | 22.53 | 21.40 | 21.44 |

| Effective bid-ask spread (bps) | ||||

| Top 200 securities by turnover | 11.37 | 11.11 | 10.58 | 10.51 |

| All Securities | 20.38 | 19.95 | 19.03 | 18.92 |

| Best depth ($) | ||||

| Top 200 securities by turnover | 744,787.13 | 909,927.85 | 764,837.55 | 837,336.70 |

| All Securities | 701,360.90 | 857,890.66 | 725,791.19 | 779,907.51 |

Note: BLD in July 2021, SYD in February 2022, CIM in Mar 2022 and MCR in Q2 2023 are excluded when computing depth metrics.

Figure 1: Market share – June quarter 2023

Figure 2: Average daily turnover

Figure 3: Average trade size by execution venue

Figure 4: Dark liquidity proportion of total value traded

Figure 5: Order-to-trade ratio

Figure 6: Intraday trading profile – June quarter 2023

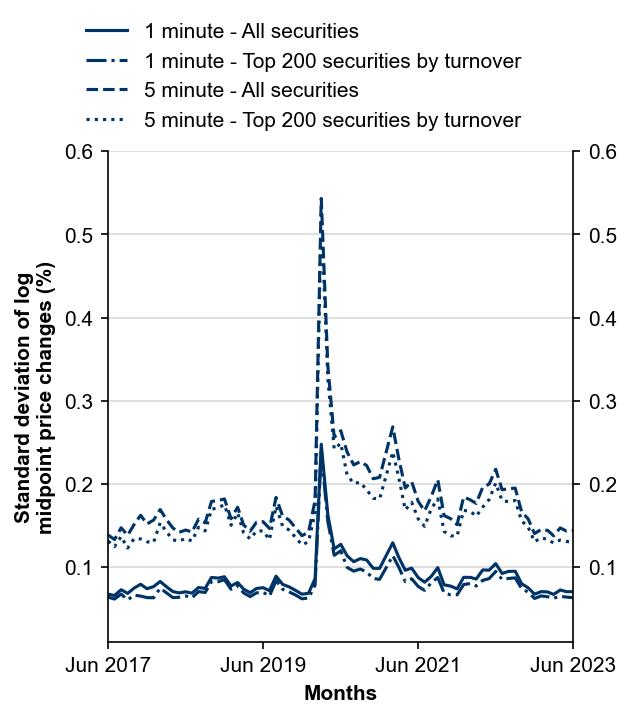

Figure 7: Intraday volatility

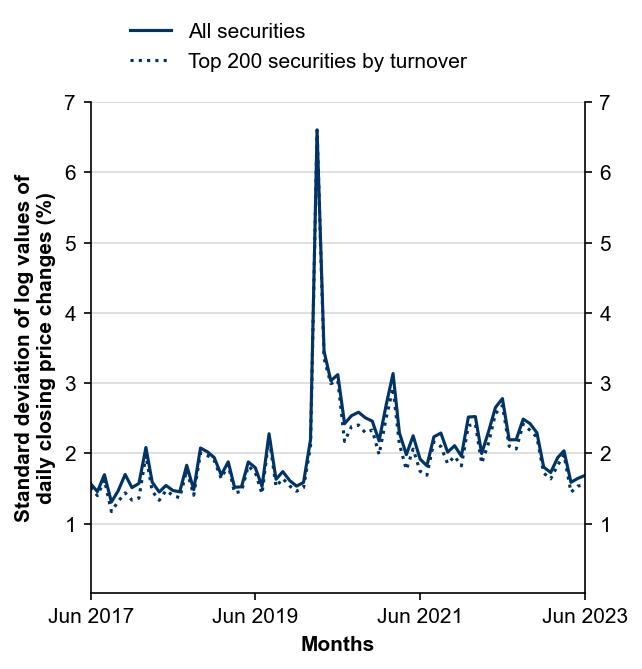

Figure 8: Interday volatility

Figure 9: Herfindahl index

Figure 10: Effective bid–ask spreads

Figure 11: Quoted bid–ask spreads

Figure 12: Depth at best bid and ask prices

Note: BLD in July 2021, SYD in February 2022, CIM in Mar 2022 and MCR in Q2 2023 are excluded when computing depth metrics.